CLAIM: Reserve Bank of Zimbabwe (RBZ) governor John Mangudya has reneged on his 2016 promise that he would resign if bond notes did not succeed.

VERDICT: The central bank governor has gone back on his word.

Researched By ZimFact Staff

THE central bank’s decision to introduce bond notes in 2016, pegged at parity to the United States dollar, sought to achieve two main objectives, to boost exports and to help ease bank-note shortages for the transacting public. The RBZ’s October 1, 2018 directive to banks to separate foreign currency accounts and bond note deposits carried a tacit admission that bond notes and electronic balances were undermining the value of foreign currency deposits.

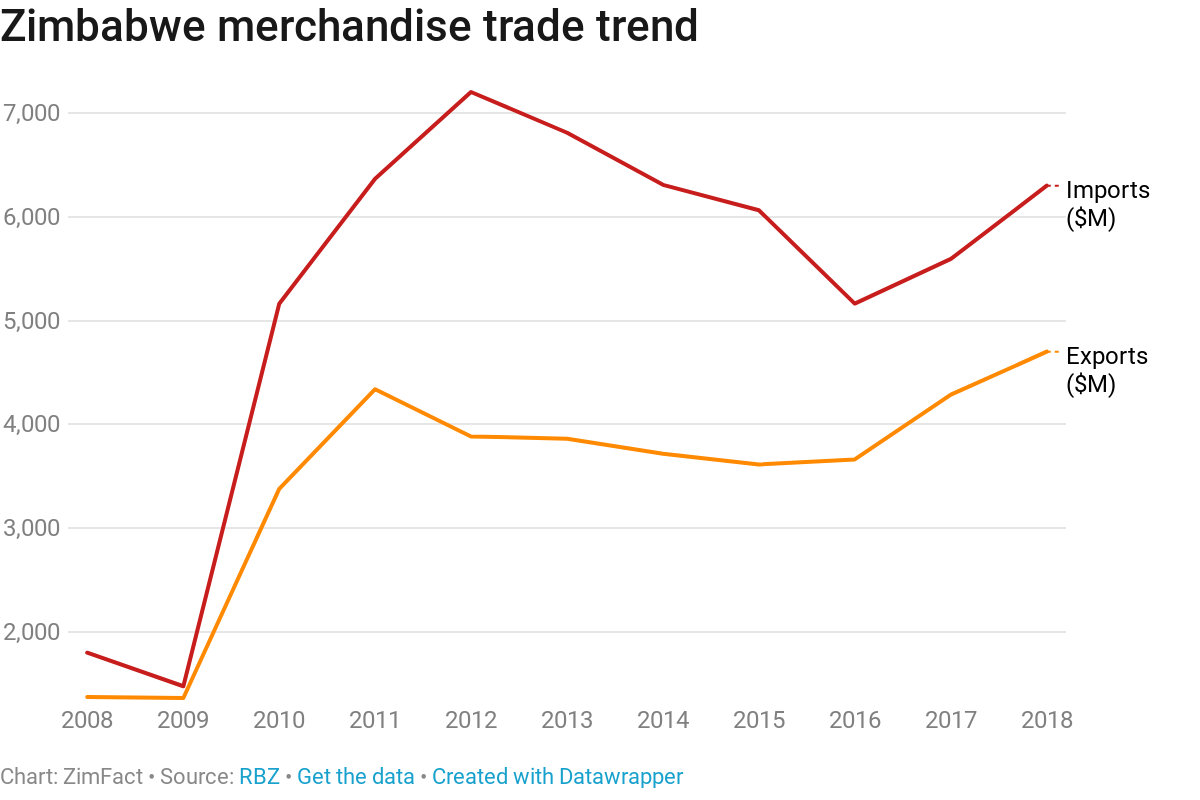

Although Mangudya has doggedly insisted that bond notes have not failed, citing export growth which he credits to the export incentive, the policy intervention has clearly failed to ease the bank note crisis.

Since Monday, there has been a social media-driven campaign for Mangudya to resign, in line with his promise.

WHAT DID MANGUDYA PROMISE?

In a May 4, 2018 release officially announcing the bond notes, the central bank said:

“The Reserve Bank has established a USD200 million foreign exchange and export incentive facility which is supported by the African Export-Import Bank (Afreximbank) to provide cushion on the high demand for foreign exchange and to provide an incentive facility of up to 5% on all foreign exchange receipts, including tobacco and gold sale proceeds.

“In order to mitigate against possible abuses of this facility through capital flight, this facility shall be granted to qualifying foreign exchange earners in bond coins and notes which shall continue to operate alongside the currencies within the multi-currency system and at par with the USD. The Zimbabwe Bond Notes of denominations of $2, $5, $10 and $20 shall, therefore be introduced in future, as an extension of the current family of bond coins for ease of portability in view of the size of the USD200 million backed facility.”

In a spirited effort to convince a skeptical public scarred by memories of the old Zimbabwe dollar, Mangudya went into overdrive to sell the bond notes.

“Give us a chance to do what is right for this economy, to put it back on track. If these policy measures fail, if the bond notes do not work out, I’m willing to resign because I am genuine about getting the economy back on track,” Mangudya was quoted by the government-controlled Chronicle newspaper.

He was to repeat his vow on a few other occasions.

HOW DID THE BOND NOTES TURN OUT?

The bond notes were introduced into the market in November 2016. Banks held $17 million worth of bond notes and coins at the end of that year.

Banks’ bond note holdings rose to $20.2 million in January 2017 and averaged $12.18 million throughout that year.

January 2018 saw banks holding the highest stocks of bond notes, $23.4 million, but that figure came down to $9 million by June, as the overall physical cash to total bank deposit ratio fell below 1%, a far cry from the widely accepted 20%.

Meanwhile, as the foreign currency crisis worsened, the bond note, which is officially pegged at parity with the United States dollar, started trading at a significant discount on the black market.

By Monday, when Mangudya announced the decision to “to eliminate the commingling or dilution effect of RTGS balances (local currency) on Nostro foreign currency accounts…in order to preserve value for money for the banking public and investors”, the bond notes were trading around 2:1 against the US dollar.

Mangudya admits he did promise to resign if the bond notes fail, but insists the currency intervention hasn’t failed.

“I said if the bond note fails to promote exports in Zimbabwe l will resign; as far as l am concerned the bond note has been successful in promoting exports. Exports have generated US$2.8 million in the first five months of this year. Gold exports have increased by 65 percent, the figures speak for themselves the bond note has not failed,” said Mangudya told ZimFact this week.

CONCLUSION:

The RBZ’s decision this week to ring-fence foreign currency deposits from electronic balances and bond notes, effectively setting hard currencies from a ‘local currency’, is the clearest official admission that the unpopular parallel currency has failed. As bank note shortages started to bite in 2016, the central bank introduced the bond notes disguised as an export incentive. Although exports, which had started declining in 2013, started to recover after the introduction of export incentives ranging from 5 percent to 10 percent, bond notes have failed to restore the banking public’s transactional convenience. Despite Mangudya’s efforts to deceptively mask this fact, he falls on his word.

Do you want to use our content? Click Here

governor John Mangudya has reneged on his 2016 promise that he would resign if bond notes did not succeed. VERDICT: The central bank governor…){kind=link}